IRS Issues Guidance on § 45Z Clean Fuel Production Tax Credit

On January 10, 2025, the Department of the Treasury (“Treasury”) and Internal Revenue Service (“IRS”) released Notice 2025-10 announcing their intent to propose regulations addressing the clean fuel production tax credit (“§ 45Z credit”) under § 45Z of the Internal Revenue Code (“Code”). The § 45Z credit is an income tax credit available to producers of domestically produced clean transportation fuel sold from January 1, 2025, through December 31, 2027. At the same time, Treasury and the IRS released Notice 2025-11 which provides initial guidance on the methodology to be used to determine the greenhouse gas (“GHG”) emissions rates for various pathways of clean fuel production which will, in turn, impact the credit amount under § 45Z. Treasury and the IRS developed both notices in consultation with the United States Department of Energy, Environmental Protection Agency, Department of Agriculture, and other federal agencies.

Notice 2025-10 includes draft text of the forthcoming proposed regulations (the “draft regulations”). The draft regulations would not be effective until published as final regulations in the Federal Register, although once published, the part of the draft regulations that requires compliance with the Notice 2025-11 emissions rate methodology table would apply retroactively to taxable periods ending on or after January 10, 2025.

On January 20, 2025, President Trump, on his first day in office, issued an Executive Order entitled “Regulatory Freeze Pending Review.” This directive pauses the publication of guidance documents in the Federal Register until reviewed and approved by an incoming Presidential appointee. This Executive Order may delay or prevent the publication of both Notices 2025-10 and 2025-11. If the Trump Administration moves forward with publication, the comment period on the draft regulations and Notice 2025-11 will provide a valuable opportunity to express support or concern with the envisioned rules for the § 45Z credit and influence its ultimate design.

Pursuant to the current versions of the notices, comments on the draft regulations set out in Notice 2025-10 and Notice 2025-11 would be due by April 10, 2025.

Background

Section 45Z provides a tax credit for the production of sustainable aviation fuel (“SAF”) and non-SAF clean transportation fuels at a qualified facility. The producer must be registered as a clean fuel producer under § 4101 of the Code and must sell the fuel to an unrelated person in a qualifying sale.

The § 45Z credit amount is calculated by multiplying the applicable amount per gallon of qualifying fuel by the “emissions factor” for the fuel. The “applicable amount” is a base amount of 20 cents per gallon for non-SAF clean transportation fuel and 35 cents per gallon for SAF. If the qualified facility satisfies certain prevailing wage and apprenticeship requirements, discussed by us here, then the “applicable amount” is multiplied by a factor of 5, equal to $1.00 per gallon for qualifying non-SAF transportation fuel and $1.75 per gallon for SAF. The § 45 credit is adjusted for inflation, pursuant to IRS regulations.

Under § 45Z(b)(1)(A), the “emissions factor” for each fuel is calculated by subtracting the “emissions rate” of the fuel from 50 kilograms of CO2e per MMBtu, and then dividing this amount by 50 kilograms of CO2e per MMBtu. Thus, the greater the emissions rate, the smaller the emissions factor and the smaller the tax credit. If the emissions rate is negative, on the other hand, the emissions factor will be above one instead of a fraction, thereby generating a credit more than $1.00 for non-SAF fuels or more than $1.75 for SAF. The draft regulations are silent on the issue of whether Treasury and the IRS have considered the negative emissions rate scenario, but the 45ZCF-GREET model appears to allow this outcome. Whether the emission rate can be negative is highly dependent on process input values.

Under § 45Z(b)(1)(B), emissions rates must be published annually by Treasury in a table that “sets forth the emissions rates for similar types and categories of transportation fuels” based on lifecycle GHG emissions as described in § 211(o)(1)(H) of the Clean Air Act. Taxpayers may file a petition for a “provisional emissions rate” (“PER”) for any transportation fuel for which an emissions rate has not been established.

For non-SAF transportation fuel, lifecycle GHG emissions must be based on the most recent determinations under the Greenhouse Gases, Regulated Emissions, and Energy Use in Transportation (“GREET”) model developed by Argonne National Laboratory or a successor model designated by the Treasury Secretary. For SAF, lifecycle GHG emissions must be calculated either using the Carbon Offsetting and Reduction Scheme for International Aviation adopted by the International Civil Aviation Organization (“CORSIA”) or a “similar methodology” that satisfies criteria under § 211(o)(1)(H) of the Clean Air Act. SAF producers must provide third-party certification of compliance with various CORSIA requirements.

These two notices come after Treasury and the IRS released Notice 2024-49 on May 31, 2024, which provided guidance on the producer registration requirements for the § 45Z credit. See this Baker Botts summary for more information about the May 2024 guidance.

Notice 2025-10

Definitions

Notice 2025-10 provides the following guidance on definitions of certain key terms in § 45Z that determine eligibility for the § 45Z credit, including:

- Facility: The draft regulations in Notice 2025-10 define “facility” as “a single production line that is used to produce a transportation fuel.” A facility includes carbon capture equipment if the capture of carbon reduces the lifecycle GHG emissions rate of a fuel. A facility may include components that are located in a different building or geographic area as other components of the facility, so long as the components function interdependently. Blending equipment is excluded from the facility definition.

- Producer: The draft regulations define a “producer” as “the person that engages in the production of a transportation fuel.” The producer does not need to own the production facility. Minimal processing like blending a fuel mixture or engaging in activities that do not result in a chemical transformation would not qualify as “production” for purposes of eligibility for the § 45Z credit.

- For alternative natural gas including renewable natural gas (“RNG”), the producer would be the person that processes the biogas “to remove water, carbon dioxide, and other impurities such that it is interchangeable with fossil natural gas.” This definition would exclude taxpayers who remove and compress conventional or alternative natural gas from pipelines because compression is not a chemical transformation. We note that the removal of water, carbon dioxide, and other impurities is also not a “chemical transformation,” but rather constitutes physical separation. Nonetheless, the IRS appears intent to distinguish compression from these other processing steps.

- Production: The draft regulations define “production” as “all steps and processes used to make a transportation fuel.” Production would begin with the “processing of primary feedstocks” and end with ready-to-sell fuel.

- Qualifying Sale: Section 45Z provides that a “qualifying sale” is a “sale of transportation fuel by the taxpayer to an unrelated person if (A) [t]he fuel is sold for use in the production of a fuel mixture by such person, (B) [t]he fuel is sold for use in a trade or business by such person, or (C) [s]uch person sells such fuel at retail to another person and places such fuel in the fuel tank of such other person.” The draft regulations provide that fuel sold for use in a trade or business must be fuel sold for use “as a fuel” in a trade or business within the meaning of § 162 of the code, signaling Treasury’s position that a sale to a buyer that will, in turn, resell or distribute the purchased fuel in bulk will not be a qualifying sale. The definition of qualifying sales in the draft regulations would also exclude sales of fuel to be used as a primary feedstock (for example, ethanol sold as a feedstock for SAF), from qualifying for the § 45Z credit. The draft regulations would clarify that a taxpayer is only eligible to claim the § 45Z credit for the taxable year in which the qualifying sale of the transportation fuel occurs. A qualifying sale may only take place once the transportation fuel is produced.

- Transportation Fuel: Section 45Z defines “transportation fuel” as fuel that is “suitable for use as a fuel in a highway vehicle or aircraft.” The draft regulations in Notice 2025-10 interpret this provision as meaning fuel that has “practical and commercial” fitness as a fuel in a highway vehicle or aircraft, or fuel that may be blended into a fuel mixture with such practical and commercial fitness. Actual use as a fuel in a highway vehicle or aircraft would not be required. For SAF, a taxpayer would meet this requirement if it sells a synthetic blending component which is then blended into a mixture described in ASTM D7566. Electricity would be excluded from the definition of “transportation fuel.” Fuel that is suitable for use in a highway vehicle or aircraft but is instead used as marine diesel fuel or marine methanol may meet the definition of “transportation fuel.”

Emissions Model

Notice 2025-10 provides the following guidance on the emissions model used to calculate the emissions rate under the § 45Z credit for non-SAF transportation fuel and SAF:

- Non-SAF Transportation Fuel: The draft regulations under Notice 2025-10 would require taxpayers to use the 45ZCF-GREET model to calculate emissions rates for non-SAF transportation fuel. The draft regulations would also designate the 45ZCF-GREET model as a successor model to GREET (as determined by the Treasury Secretary).

- The Notice asserts that the 45ZCF-GREET model both represents the “most recent determinations” under the GREET model referenced in the statutory text (though the 45ZCF-GREET did not exist when the law was passed) and is a successor model to GREET as determined by the Treasury Secretary. The Notice alleges several deficiencies in the “R&D” GREET model that make it inadequate for § 45Z purposes, even though this was the only version of the GREET model that existed when the statute was passed. The “R&D” label was added only after the IRS began to implement the Inflation Reduction Act.

- The first version of the 45ZCF-GREET model and an accompanying user manual were released on January 15, 2025, and can be accessed here. See the 45ZCF-GREET section below.

- Like other iterations of GREET established for purposes of the Inflation Reduction Act, 45ZCF-GREET contains both fixed assumptions that the IRS calls “background data” and customizable inputs called “foreground data.” The background data cannot be modified even if the producer has evidence that the data is not representative of the user’s production process.

- Comparison to § 45V: For hydrogen used as a production input for transportation fuel, the draft regulations require the use of the 45VH2-GREET model. Notably, the 45V regulations, discussed by us here, allow a developer to elect to use the 45VH2-GREET model available at the time construction began to calculate emissions for the 10-year credit period. In contrast, the § 45Z proposed guidance requires that the most current 45ZCF-GREET version available in the year the § 45Z credits are generated be used. Thus, there is uncertainty about what the § 45Z credit amount will be for the duration of the credit period. This uncertainty may make largescale investments, like those in SAF projects, more difficult.

- SAF: The draft regulations would require taxpayers to use the most recent version of the CORSIA Default Life Cycle Emissions Values for CORSIA Eligible Fuels (“CORSIA Default”), the CORSIA Methodology for Calculating Actual Life Cycle Emissions Values (“CORSIA Actual”), or the 45ZCF-GREET model, as directed by the emissions rate table, to determine emissions rates for SAF. Notice 2025-10 explains that the 45ZCF-GREET model is a “similar methodology” to CORSIA because like CORSIA, it evaluates emissions throughout the full fuel lifecycle.

- Climate-Smart Agriculture: Treasury and the IRS intend to propose rules in the future regarding the calculation of lifecycle GHG emissions benefits associated with certain climate-smart agriculture practices for corn, soybeans, and sorghum. However, the climate-smart agriculture provisions are not described in the draft regulations nor addressed in detail in the Notices, although Treasury and the IRS state that they anticipate requiring third-party certification of crops using climate-smart agriculture practices.

- On January 16, 2025, the U.S. Department of Agriculture released a prepublication version of an interim rule that establishes guidelines for quantifying, reporting, and verifying GHG emissions resulting from implementing climate smart agricultural practices for corn, soybeans, and sorghum. The following practices are identified as climate-smart agricultural practices: no-till, reduced till, cover crops, nitrification inhibitors, split in-season nitrogen application, and no Fall nitrogen application. The GHG emissions associated with a defined set of climate-smart agricultural practices will be quantified using the USDA Feedstock Carbon Intensity Calculator (“USDA FD-CIC”) once it is finalized. USDA intends for these guidelines to be used in international, national, or state clean transportation fuel policies. Treasury and the IRS may incorporate USDA’s climate-smart agriculture interim rule in its future guidance.

45ZCF-GREET

The 45ZCF-GREET model calculates GHG emissions of various fuel products, specifically, ethanol, renewable diesel (“RD”), SAF, biodiesel, and hydrogen. The key inputs for the calculation include feedstock selection, electricity source, hydrogen carbon intensity (“CI”) where applicable, and natural gas and/or RNG inputs. Carbon capture is available as an input for ethanol pathways and gasification with Fischer-Tropsch synthesis pathways.

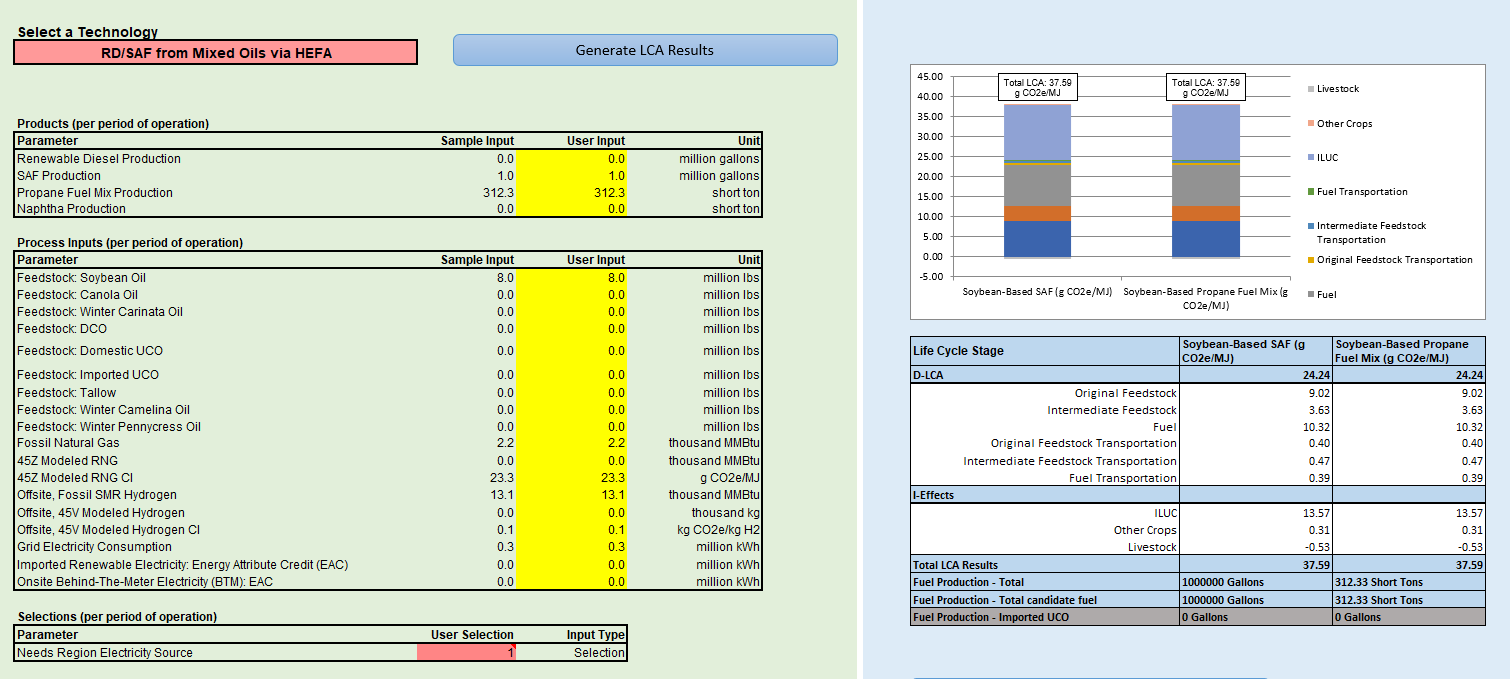

Inputting data into the 45ZCF-GREET model begins with using a dropdown menu to select the fuel type, production process, and feedstock being modeled. The options available in the dropdown menu are summarized in Table 1 below. The left side of Figure 1 displays the input parameters (foreground data) that must be entered after a high-level option is selected in the dropdown menu, in this case for SAF/RD produced from mixed oils via hydrotreated esters and fatty acids (“HEFA”). Hydrogen can be modeled as a fuel product or as a process input where applicable, such as in the production of HEFA. It is worth noting that the emissions rate result can be negative but is highly dependent on the RNG and hydrogen process input values. The right side of Figure 1 illustrates an example of the model’s output.

The variables within the 45ZCF-GREET model that are fixed or locked down as background data include:

- All crushing facility data for crop-based oil, such as soybean crush plant electricity and chemical inputs.

- All transport distances for feedstock, intermediates, and final fuel products are fixed at the national average values.

- All farm-based data is fixed as conventional farming practices.

- Non-liquid fuel co-products and co-product yields.

- Emissions associated with induced land use changes when cropland is brought into production or market-driven shifts in the type/location of cropland occur.

Table 1: Options Available 45ZCF-GREET Master Dropdown Menu

| # | Fuel / Energy | Fuel Product | Process Input | Technology | Feedstock | Comment |

| 1 | Ethanol | X | Fermentation | Corn + Sorghum, Corn, Sorghum, Brazilian Sugarcane, Corn Stover | No wet milling pathway. U.S. crop production only unless noted. | |

| 2 | RD/SAF | X | HEFA | Mixed oils, soybean oil, canola oil (U.S. or Canada), winter carinata, winter camelina oil, DCO, UCO, tallow (U.S. only), pennycress |

U.S. crop production only unless noted. If imported used cooking oil (“UCO”) is mixed with domestic UCO, the imported volume must be entered into the model but are excluded from the fuel LCA calculation. |

|

| 3 | RD/SAF | X | Alcohol to Jet (ATJ) | Domestic or Brazilian Ethanol | ||

| 4 | RD/SAF | X | Gasification and Fischer-Tropsch | Corn Stover | ||

| 5 | Biodiesel | X | Transesterification | Mixed oils, soybean oil, canola oil (U.S. or Canada), winter carinata, winter camelina oil, DCO, UCO, tallow (U.S. only), pennycress | If imported UCO is mixed with domestic UCO, the imported volume must be entered into the model but is excluded from the fuel LCA calculation. | |

| 6 | Hydrogen | X | X |

Fossil SMR or CI Modeled per GREET45V or PER On-site hydrogen generation is reflected in the overall site mass and energy balance which does not appear to recognize CCUS |

||

| 7 | RNG | X | Anaerobic digestion and biogas upgrading | Landfill gas, animal manure, wastewater sludge | CI Modeled per GREET45Z. RNG CI can be negative. | |

| 8 | Electricity | X | Select from 15 U.S. grid regions, imported renewable (EAC), and/or behind-the-meter generated (EAC) |

Figure 1: 45ZCF-GREET LCA example for HEFA SAF from mixed oils = 37.59 gCO2e/MJ

To see image full size: right click and open in a new tab.

Anti-Stacking

The draft regulations presented in Notice 2025-10 also would clarify the prohibition on claiming multiple types of tax credits for a single production process (referred to as “credit stacking”). Section 45V prohibits claiming the § 45Z credit in the same taxable year that the § 45V or § 45Q production credit is claimed with respect to production from the same facility. The draft regulations would confirm that entities may alternate between claiming the § 45Z credit and these other credits in different taxable years. An entity that claims the § 48(a)(15) clean hydrogen investment tax credit with respect to a facility, on the other hand, is forever barred from claiming the § 45Z credit for the same facility.

Substantiation, Recordkeeping, and Certification

Additionally, the draft regulations include a number of recordkeeping and substantiation requirements for fuel producers. For example, producers must maintain records related to primary feedstocks, how emissions rates were calculated, and fuel testing, among many other topics. Non-SAF transportation fuel producers that receive certifications consistent with the SAF certification provisions described below would qualify for a safe harbor from emissions rate substantiation requirements.

The draft regulations include certain third-party certification provisions for SAF producers. The regulations would accept certifications from the International Sustainability and Carbon Certification (“ISCC”), Roundtable on Sustainable Biomaterials (“RSB”), and other sustainability certification schemes approved by the International Civil Aviation Organization (“ICAO”) if CORSIA Default or CORSIA Actual is the selected emissions rate methodology, and verification bodies approved by the American National Standards Institute or under the California Low Carbon Fuel Standard program if the 45ZCF-GREET model is used.

Concerned about improper identification of used cooking oil feedstocks from foreign sources, Treasury and the IRS are considering additional substantiation and recordkeeping requirements for imported used cooking oil feedstocks. Until such requirements are promulgated, the 45ZCF-GREET model does not contain a pathway for imported used cooking oil.

Notice 2025-11

Notice 2025-11 establishes the initial table of emissions rate methodologies used to calculate the § 45Z credit. This table is in response to the statutory requirement that the Treasury Secretary annually issue a table “which sets forth the emissions rate for similar types and categories of transportation fuels.” The table, copied below as Appendix A, includes fuel types, pathways, and primary feedstocks associated with the fuel.

Rather than actually assigning emissions rates to these categories, the table specifies that fuel emissions rates are to be calculated using the most recent determinations under 45ZCF-GREET for non-SAF transportation fuel; the most recent version of CORSIA Default, CORSIA Actual, or 45ZCF-GREET for SAF; or the 45VH2-GREET model for hydrogen. The IRS requests comments on how fuel pathways under the Environmental Protection Agency’s Renewable Fuel Standard Program could be adapted for the emissions rate table, and whether additional fuel categories currently in commercial use should be added to the table.

For fuels, feedstocks, and pathways not addressed by the emissions rate table, the IRS indicates that it plans at a later date to establish a procedure for applying for a PER. Under the envisioned PER process, the Department of Energy will provide an emissions value based on applicant-submitted data and its analytical assessment of the lifecycle GHG emissions rate associated with the fuel. Producers may apply for PERs only for novel fuels, feedstocks, or pathways not addressed by the emissions rate table. The IRS will not consider a PER application that is submitted because a producer disagrees with underlying assumptions in the 45ZCF-GREET model or calculation approaches in the applicable model. The IRS will not accept requests for PER determinations until the guidance is published.

We will continue to monitor the Inflation Reduction Act guidance initiatives from the IRS and Treasury and will provide further updates as guidance is released. In the meantime, Baker Botts would be pleased to assist you in your analysis of clean energy tax incentive matters.

ABOUT BAKER BOTTS L.L.P.

Baker Botts is an international law firm whose lawyers practice throughout a network of offices around the globe. Based on our experience and knowledge of our clients' industries, we are recognized as a leading firm in the energy, technology and life sciences sectors. Since 1840, we have provided creative and effective legal solutions for our clients while demonstrating an unrelenting commitment to excellence. For more information, please visit bakerbotts.com.