Energy Private Capital Market Review

General Private Equity

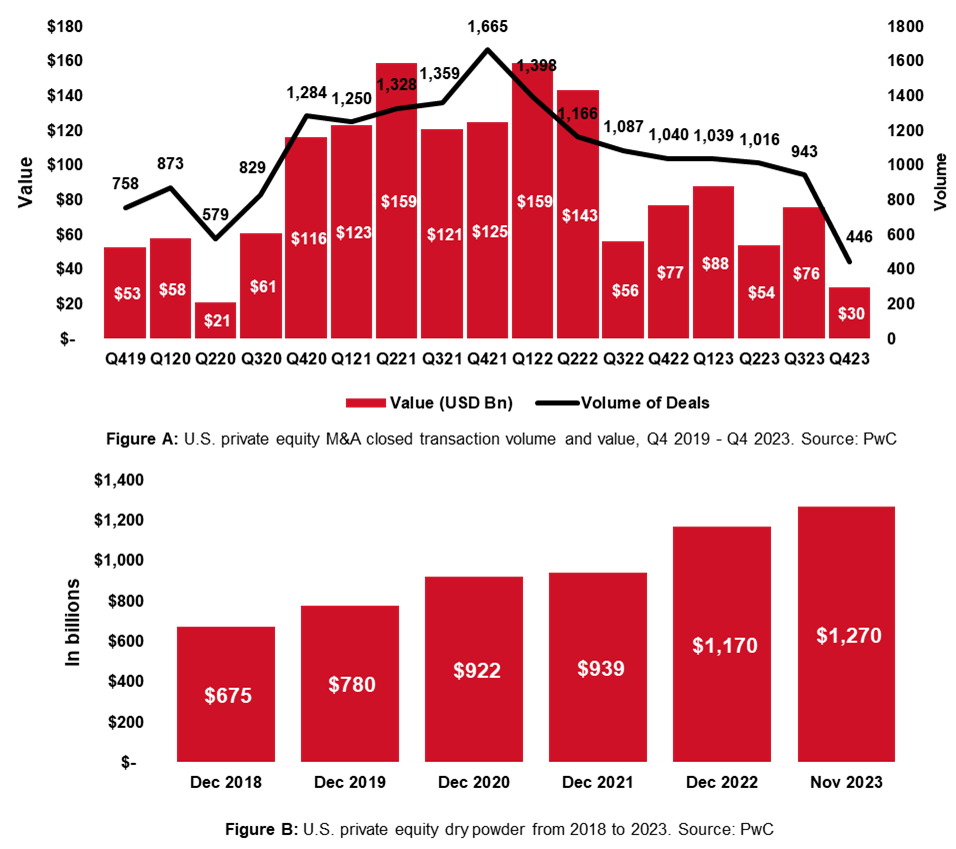

Rising interest rates created significant disruptions in the private equity industry in 2022 and 2023, with increased cost of debt having knock-on effects on valuations of target companies. At the same time, the industry has amassed a large amount of dry powder (Figure B), which is pushing firms to innovate and adapt their deal structures to continue making deals. In 2024, we believe several trends are expected to persist or emerge in the PE landscape:

- Continued strength of the middle market, which has seen more activity than the upper market due to less reliance on debt financing. In 2023, the middle market accounted for 62% of the total deal value, up from 54% in 2022.

- Greater room for strategic acquirers to win deals due to their lower reliance on debt and more conservative valuation expectations. In 2024, an uptick is expected in stock-for-stock transactions and other unique deal structures that do not require debt financing. In 2023, stock-for-stock transactions accounted for 17% of total deal value, up 12% from 2022.

- Increased use of earn-outs and other deferred consideration to bridge the gap on valuation between buyers and sellers. In 2023, earn-outs represented 23% of total deal value in 2023, up 18% from 2022.

- Growing need for secondary buyers of private fund interests due to the shortage of exit opportunities, which has left an estimated 75% of private portfolios net cash-flow negative. The average holding period for private equity investments increased to 6.2 years in 2023, up from 5.4 years in 2022.

- Artificial intelligence remains a major force reshaping markets and the broader economy, with significant near and medium-term investment opportunities in companies whose products and services can easily and effectively employ AI applications.

|

Despite potential momentum reflected in these expected trends and overall historical strength, pessimism still looms in the PE space. The Wall Street Journal states that PE firms are bracing for a continued period of lean fundraising through 2024, as interest rates stagnate the M&A market and diminished IPO opportunities hinder recoveries and exit opportunities. While energy sponsors are familiar with zombie portfolio companies and zombie funds resulting from by cyclical and structural changes, these phenomena are expected to become pronounced broadly in other industries.

While Fed Chair Jerome Powell has indicated that the Fed is unlikely to raise rates further, he and other Fed officials have also suggested that any rate declines would occur gradually, stamping out the possibility of a “quick fix” this year. As such, investors will continue to turn to alternative capital sources such sovereign wealth funds and family offices, both of which have remained strong among the broader group of LPs and PE sponsors despite macroeconomic headwinds.

Energy Outlook

The energy industry underwent significant changes in the past year, driven by macroeconomic, geopolitical, regulatory and technological factors that have shaped the demand and supply of energy commodities and services. These changes have created both challenges and opportunities for sponsors. In 2024, energy sponsors can expect to see several trends that are expected to influence their investment decisions and performance such as:

- Increased focus on low-carbon energy transitions and ESG considerations: The global momentum toward achieving net-zero emissions and aligning with the Paris Agreement has accelerated the deployment of renewable energy and clean technologies despite lagging financial return profiles to date. ESG criterion have been adopted by investors, regulators and consumers. Sponsors have been increasingly exploring and investing in low-carbon energy opportunities including generation (not as much anymore), battery storage (hot), carbon capture (better) and “picks and shovels” suppliers (best), as well as integrating ESG factors into their portfolio management and value creation metrics. However, sponsor investments continue to face valuation volatility, supply chain bottlenecks, lowered debt capacity and technological risks. While attitudes towards ESG investing remain widely positive, the increased interest rate environment and trends away from globalization have resulted in the rethinking of some valuations.

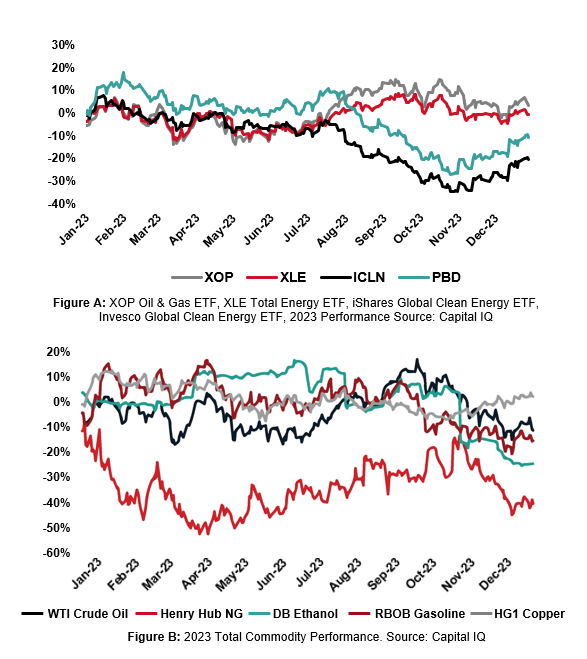

- Reticent return to traditional energy: The improved general sentiment and fundraising environment for traditional energy during 2023 suggested that a portion of the institutional investment community who exited traditional energy from 2020 to 2022 may have been driven by financial rather than social reasons. The lagging performance of the XOP in 2023, however, may keep those investors on the sidelines. While traditional energy enjoys a much healthier leverage profile today relative to that from the previous decade, whipsaw commodity performance and overcommitment of capital budgets still has investors reticent. Energy private credit will continue to be the main focus of traditional sponsors this year.

- Diversification of deal types and sources of capital: The higher interest rate environment and the higher cost of debt have impacted deal economics of PE transactions and alternative capital sources. The middle market is deluged with competing term sheets. The saturated private credit market is replacing the prior role fulfilled by bank facilities. Sponsors are now more selective and creative in their deal sourcing and structuring, at a price.

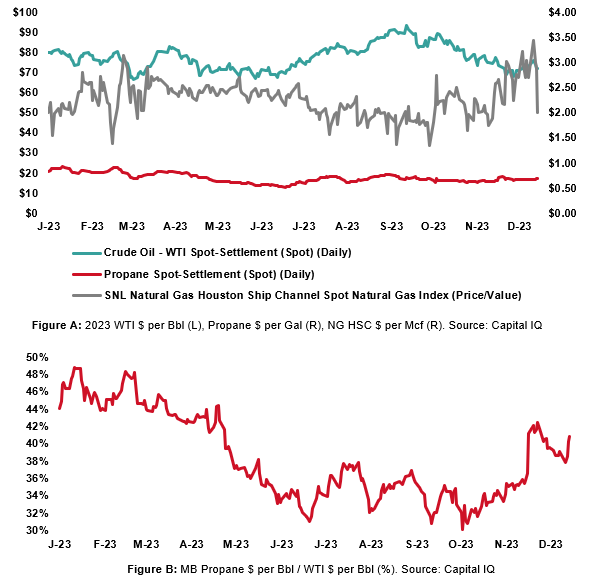

- Commodities: After rising inflation boosted commodities in 2021 and 2022, this trend reversed in 2023 as inflation and economic growth both slowed. This was reflected in the Bloomberg Commodity Index (BCOM) increasing 27.1% and 16.1% in 2021 and 2022, respectively, before plunging downward 7.9% in 2023. Energy sponsors are responding to this volatility by harvesting pre-2022 vintage investments while simultaneously deploying new capital into natural gas-weighted opportunities which are at a cyclical low. Bloomberg has highlighted economic conditions in China, geopolitical conflicts and inflation’s direction as the major commodity drivers for 2024. The crude oil markets reflect a geopolitical risk premium which has contributed to sending Brent crude prices towards $90 per barrel. At the same time, with a rising natural gas “drilled but uncompleted” well (DUC) count, domestic gas fundamentals face challenges against constructive normalization at Henry Hub prices in the short-term.

|

E&P Market Commentary

2023 brought some stability to the traditional energy M&A market as oil settled into a long-term price structure above most tier 1 and tier 2 break-even levels, however, natural gas and natural gas liquids (NGLs) prices were hammered towards cyclical lows which decimated gas deal activity during the second half of the year. Generally, M&A was strong with 110 deals closed which were valued at an aggregate $179.2 billion. Deal activity remains strongest in the Permian basin as the proven resource and infrastructure complex supports continued new investment, although asset prices and activity in the Eagle Ford suggest that capital will flow aggressively towards any area that presents low risk-drilling, well understood geology and market access.

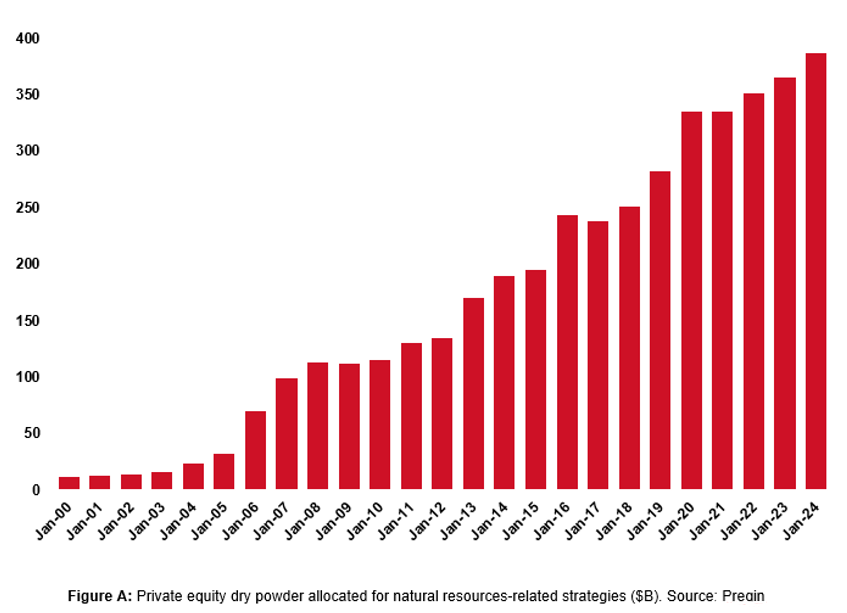

Valuations across basins are experiencing a very divergent bifurcation as value rushes back towards high quality undeveloped properties after many years of inattention. In both public and private M&A, the market is placing a premium on undeveloped locations. The anxiety of publicly traded E&Ps with respect to their depth of inventory is palpable. As a result, companies and asset packages with significant undeveloped upside enjoy a sellers’ market and would be expected to trade significantly above PDP PV-10, with excess value attributable to acreage. The prevailing theorization of acreage value is a drilling risk-adjusted discounted present value on inventory based on the buyer’s drilling schedule. In contrast, wellbore and low to no-upside deals trade at a wide discount rate, as buyers must cleave all of their base case return from the declining production value. Facing a new buyer, that buyer is both creating diseconomies of scale with a separate management team and requiring a post-G&A return in excess of 20%, which manifests itself in the bidder’s PDP discount rate. For this reason, mature and scaled E&Ps with credit facility capacity have emerged as the buyers of preference for PDP assets, and PE dry powder continues to build.

|

What some may call a bifurcation in value, others may simply call a PUD premium, although one struggles to find a consistent discount rate applied to PDP. These developments have created a number of interesting observable deal dynamics:

- The allocation of value across the properties under the PSA becomes a highly material transaction item, shifting from its traditional role as a schedule delivered by the buyer. Allocation of value can become disruptive to a transaction if it suggests that a seller may be able to obtain better pricing for its undeveloped properties elsewhere.

(a.) Value allocation to PUDs also creates more complexity to the operation of tag-along and preferential rights, and the consummation of transactions inclusive of third-party rights, leading buyers deeper into diligence to identify these material issues earlier in deals and strategies to accommodate them.

- Acquisition financing has resurged to become a popular way for credit funds to participate in the market, particularly in PDP-heavy transactions. The entry point on PDP collateral remains relatively cheap. Alternative financing is generally as available and competitive to E&Ps as it has been in recent cycles (at a price) as financing sources compete to deploy capital into the current interest rate environment.

(a.) Market practices regarding bring-down title thresholds between acquisition financing players (PDP-based) and buyer-borrowers (PDP + PUD) are divergent where the buyer-borrower will have a higher scope of defect in a PSA title defect mechanic (and thus more sensitive closing defect threshold) than the closing conditions to acquisition financing.

(b.) Financing covenants lag behind M&A market practices in covenant lack of value attribution to undeveloped properties. This suggests credit participants may be forced to become more aggressive and flexible to compete.

- Good title to undeveloped properties becomes a new source of risk to deals as the “land” diligence function has been de-emphasized over the last decade and undeveloped properties previously did not receive significant value attribution as they do today.

- The technical methodology of reserve reports to limit PUD attribution to immediate adjacencies to existing PDP wells does not reflect market valuation practices and may obfuscate valuation information. Market players are laying down drilling locations across the observable reservoir and the market is paying for these “PUDs,” calling into question the role of technical PUDs as an anchor valuation framework for undeveloped value in both M&A and financings.

- Representation and warranty insurance continues to be a popular means of addressing post-transaction risk, but it is more difficult to satisfy due diligence requirements in a transaction with large undeveloped value attribution because the scope of diligence to satisfy an insurer may be more extensive than prevailing industry practices.

|

Setting transaction trends aside, the impact of natural gas and NGL price declines simply cannot be understated. The market went from a premium in 2022 to a low point in a year where myriad Gulf Coast LNG in-service dates approached. When Henry Hub nosedives and remains in a doldrum like this, E&Ps take action. The reality in the “field” is worse than Hub pricing as no-LA, non-Gulf Coast basis further cuts into price realizations. As we are all presently witnessing, gas operators will look to every tool in their capital and contractual arsenal to preserve value, including steps to:

- Lay down rigs, suspend the development program and take aggressive positions on their drilling and completion contracts to avoid financial penalties for doing so.

- Renegotiate midstream and marketing contracts with counterparties to preserve and improve margin. These actions may take the form in-kind payment or fee relief in exchange for future obligations.

- In the most extreme cases, shut down a field or a portion of it in a bid to preserve value or re-trade midstream contracts. The latter approach should be heavily scrutinized for contractual consequences and long-term relationship damage with midstream counterparties.

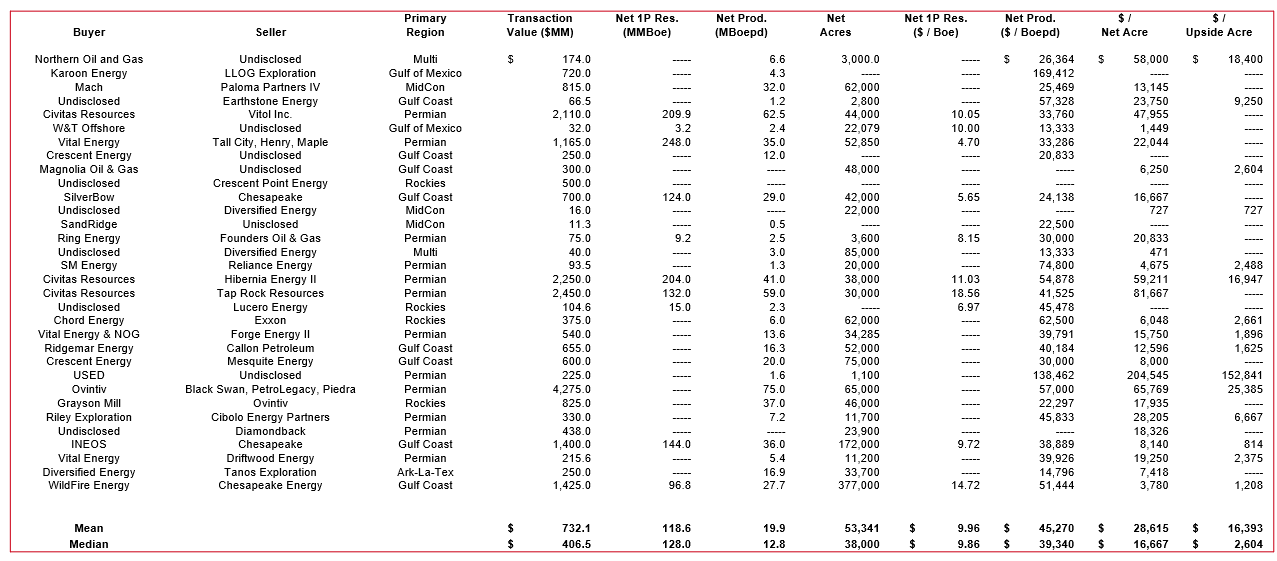

2023 E&P Working Interest Deals (Stephens)

|

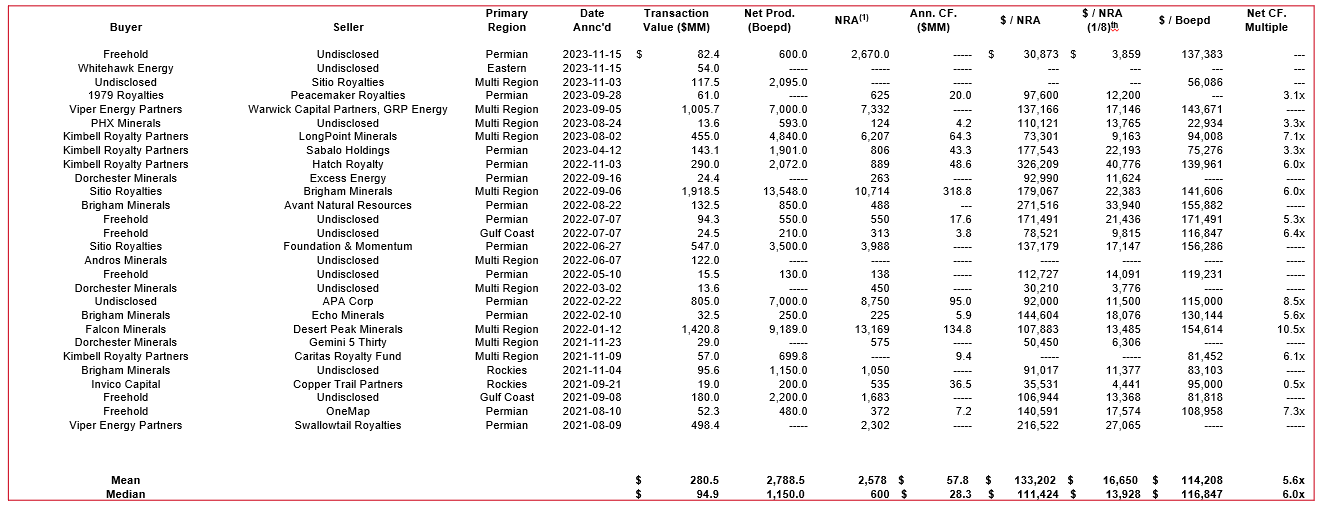

2021-23 Mineral & Royalty Deals (Stephens)

|

Energy Transition Outlook

According to PitchBook’s Q4 2023 Clean Energy report, the quarter saw $3.0B in VC funding for clean energy technologies, a 17.0% decrease from Q3 2023. Deal count increased over such period from 152 to 162. Analysts note that grid infrastructure technologies raised the most funding of the clean energy segments, turning in $1.1B of deal value compared to the $965M raised by intermittent renewable energy sources. During 2023, lower deal volumes were partially driven by the volatile economic environment absorbing higher interest rates, continued inflation and bank failure uncertainties. While some of these constraints are likely to continue into 2024, clean and renewable energy will be a major focus of energy sector private investment in 2024 as companies and governments seek to make progress on global energy transition.

While all types of clean energy investment are being considered, several have emerged as potentially lucrative. Increased manufacturing capacity has helped bolster megadeals in the battery storage and hydrogen spaces while increased global interest in renewable electricity has driven significant investment in Asian solar PV manufacturing companies. Government support for renewable energy cannot be overlooked as a factor either: for example, the EU has formalized a timeline of targets for the aviation industry to incorporate sustainable aviation fuels (SAFs) and the U.S. announced that seven regional clean hydrogen hubs will receive $7B in funding through the Bipartisan Infrastructure Law. Combined with the Inflation Reduction Act, energy transition sponsors have significant incentives to invest in energy infrastructure, which makes it EY’s #2 pick for its top five private equity trends in 2024.

Notably, while much of the funding for the U.S. regional clean hydrogen hubs will be allocated to public companies, it opens doors for further investment in private hydrogen technology companies. Clean hydrogen currently has the largest gap between announced and realized investments: more than $50B and less than $1B, respectively. This has been attributed by multiple sources, such as the International Energy Agency, to escalating equipment and financial costs, which have been exacerbated by high interest rates and inflation. In a December 2023 report on private equity-backed renewables, S&P Global predicted that these headwinds would continue to impact renewables investments and highlighted challenging return-on-investment metrics as an additional factor. Yet, S&P Global also predicted in January 2024 that private equity-backed renewable energy dealmaking would begin to rebound this year despite those headwinds, citing the closing Brookfield Infrastructure Fund V. This fund, which will partially focus on decarbonization and has already made renewables investments, closed with a record $28B of commitments in December 2023 – above its $25B target. Should interest rates and inflation abate over the year, it could be easier for sponsors to meet investment hurdles down the road. As such, renewable energy and energy transition remain as a focus for many sponsors.

ABOUT BAKER BOTTS L.L.P.

Baker Botts is an international law firm whose lawyers practice throughout a network of offices around the globe. Based on our experience and knowledge of our clients' industries, we are recognized as a leading firm in the energy, technology and life sciences sectors. Since 1840, we have provided creative and effective legal solutions for our clients while demonstrating an unrelenting commitment to excellence. For more information, please visit bakerbotts.com.